The White House just turned your retirement account into collateral damage in a reckless trade war. By attempting to freeze Canadian assets, the administration triggered a $2.3 trillion global bank run, permanently crippling the US dollar and leaving the American taxpayer to foot a catastrophic bill.

The Empty Vault and the Executive Overreach

Over the weekend, the president of the United States invoked the International Emergency Economic Powers Act—a heavy-handed tool historically reserved for rogue states like Iran and North Korea. The target this time was not a constitutional adversary, but Canada, a Five Eyes intelligence ally with whom we share a 5,525-mile undefended border. The administration sought to freeze $89 billion USD in Canadian government and corporate assets held in American banks, justifying this financial warfare under the guise of a trade dispute. It was a staggering betrayal of free-market liberty and international transparency. But the White House policy architects made one fatal miscalculation: the vault was empty. Under the direction of former central banker Mark Carney, Canada had spent 90 days quietly executing Operation Sovereign Shield, a methodical transfer of $77 billion out of American jurisdiction. The intended hostage had already escaped. But the true horror for the American economy was not the embarrassment of an empty vault; it was the financial bloodbath that was about to begin.

Capitol Hill Reaction and the Partisan Divide

The Capitol Hill reaction was immediate and fiercely divided. Republicans condemned the executive order as a gross violation of property rights and a catastrophic overreach that threatens the bedrock of American economic liberty. They warned that this weaponization of the financial system would be the defining issue of the 2026 Midterms.

Meanwhile, Democrats scrambled to defend the White House policy, attempting to spin the trade dispute as a defense of domestic industries, even as they privately panicked over the spiraling economic fallout. The partisan shouting match, however, completely missed the broader constitutional crisis. By treating foreign assets as political leverage, the executive branch abandoned the foundational American promise of a safe, neutral marketplace. As politicians bickered over optics, foreign capitals were already executing a maneuver that would permanently alter the balance of global power.

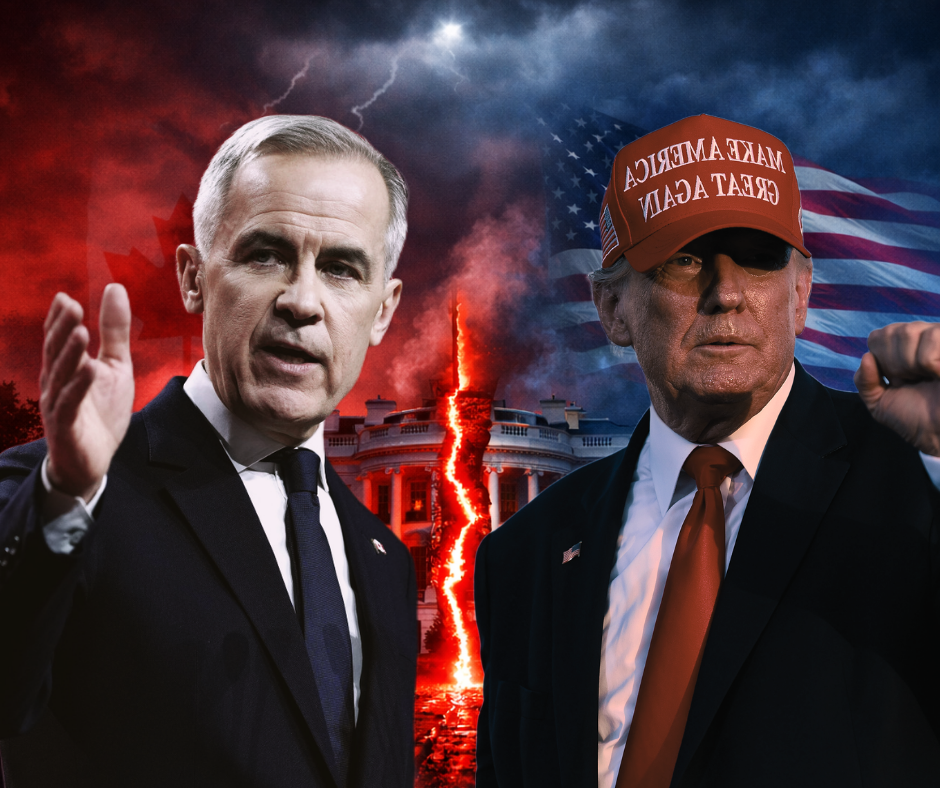

“Not a Deposit. It is a Hostage.”

When Mark Carney stepped to the podium in Ottawa, he did not just counter the American offensive; he dismantled the illusion of American financial supremacy. Revealing that only $12 billion in residual assets remained trapped, Canada instantly invoked its own emergency powers, freezing $143 billion in American assets held in Canadian institutions. This 12-to-1 ratio was a devastating counter-strike. Yet, it was Carney’s message to the international community that truly shattered the paradigm. He declared that if the United States would weaponize its banking system against its closest ally, no nation’s wealth was safe. He delivered a sentence that will haunt American taxpayers for generations: “Your money in American banks is not a deposit. It is a hostage.” The market’s reaction was instantaneous, brutal, and targeted directly at the foundational pillars of American wealth.

A $340 Billion Bloodbath on Wall Street

The Dow Jones began a freefall the moment those words hit the wires. American bank stocks, the very engines of our domestic economy, led the collapse. JPMorgan Chase dropped 9 percent, Bank of America fell 12 percent, and Citigroup cratered a staggering 14 percent.

In a single trading session, the banking sector lost over $340 billion in market capitalization. This was not just a bad day on Wall Street; it was the rapid evaporation of the American taxpayer’s 401(k) accounts, pension funds, and institutional stability. Analysts immediately drew terrifying parallels to the 2008 financial crisis. Yet the most terrifying consequence of this executive hubris is not what happened on Wall Street, but what is happening right now in sovereign vaults from Oslo to Riyadh.

The Oracle’s Warning and the 2026 Midterms

The panic reached a fever pitch when Warren Buffett addressed the nation from Omaha. The Oracle revealed that Berkshire Hathaway had been quietly reducing its exposure to US bank stocks for the past 12 months, anticipating the inevitable collapse of a system that substitutes constitutional neutrality for political weaponization. Buffett called the freeze the most self-destructive financial decision by an American president since Richard Nixon closed the gold window in 1971. He branded the move as “spite disguised as strategy.” When the world’s most successful investor publicly declares that political weapons are poor long-term investments, the electorate listens. The economic devastation sparked by this single executive order will undeniably shadow every debate leading into the 2026 Midterms.

The $4.7 Trillion Global Exodus

Within 48 hours of the freeze, 11 sovereign wealth funds—including Norway’s massive $1.6 trillion fund, Saudi Arabia’s Public Investment Fund, and Singapore’s GIC—announced formal reviews of their US exposure. A staggering $4.7 trillion is now actively seeking the exits. The European Central Bank is accelerating a Euro-based alternative to dollar clearing, while China gleefully expands its Yuan settlement agreements.

The world is realizing that the US dollar is no longer a global public good; it has become an American weapon.

The Final Cost to the American Taxpayer

The United States spent decades building a financial system grounded in liberty, transparency, and the rule of law. That trust was our most valuable asset, far more potent than any military capability. By freezing Canadian assets, the president did not punish Ottawa; he punished 330 million Americans. As global demand for dollar-denominated assets permanently declines, the cost of borrowing for American businesses and homeowners will skyrocket. The dollar is worth exactly what the world’s trust in American institutions is worth. Today, that trust is broken, and the American taxpayer is left paying the ultimate price.

Editorial Note: The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of any agency or organization. This content is intended to provide diverse perspectives on current events.